18 hours ago

16

18 hours ago

16

By MATTHEW HOLT

I know my many fans love me delving into the world of why we get seemingly incorrect trivial bills in health care, and what they all mean. The long telenovella of the $39.94 bill from Labcorp is as yet stalled with One Medical apparently resubmitting the original claim with the new preventative codes on it. But even though I am continuing and expanding my role as a difficult patient this year, there are still some blasts from the past that won’t quite leave.

This particular one concerns some rather unpleasant dermatology issues. For many years I had an unpleasant small sore/lesion on my leg that never quite healed. Then I started getting a few more that started as zits and never quite left. My wise PCP Andrew Diamond at One Medical told me to use some antibiotic wash and referred me to a dermatologist. Unfortunately the one I was referred to was out of network for the Blue Shield HMO I was in, but one request back to One Medical and I was both sent to a dermatologist in my network and got a pre-auth in the mail from Blue Shield to go see him!

Dr Cristian Gonzalez took a quick look at my leg, decided what the problem was, and proceeded to inject, freeze and attack my various lesions. He then prescribed a cheap topical steroid for me to use, and basically after 4 visits over the summer and Fall, my legs went back to resembling a baby’s bottom–well more or less.

For each specialty visit Blue Shield had a co-pay of $85 per visit, which I handed over using my HSA card. One time the front desk said I had a balance, but when I asked them what it was for they told me it was a mistake. Until this week.

Some 4 months after my last visit I got a bill in the mail for $51.96

Given that I had made a co-pay of $85 each time, this seemed a little odd. So I took a look at my Blue Shield EOBs. (BTW they are back online, you may recall they vanished when Blue Shield cancelled and then changed my plan but the Internet never forgets….)

There a curious anomaly began to play out. Each visit generated three identical claims and three more or less identical EOBs.

All for the same amount, with different claims, two appear to have been paid, one not. So that doesn’t make a lot of sense. But it seems that each visit paid ballpark $255 and possibly another $85 from me on top.

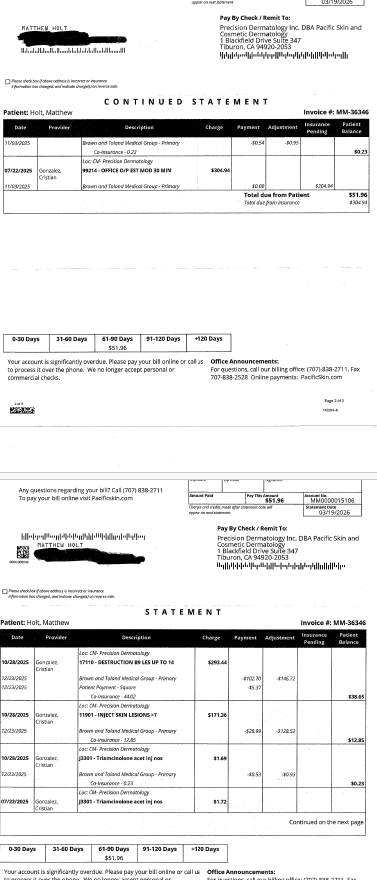

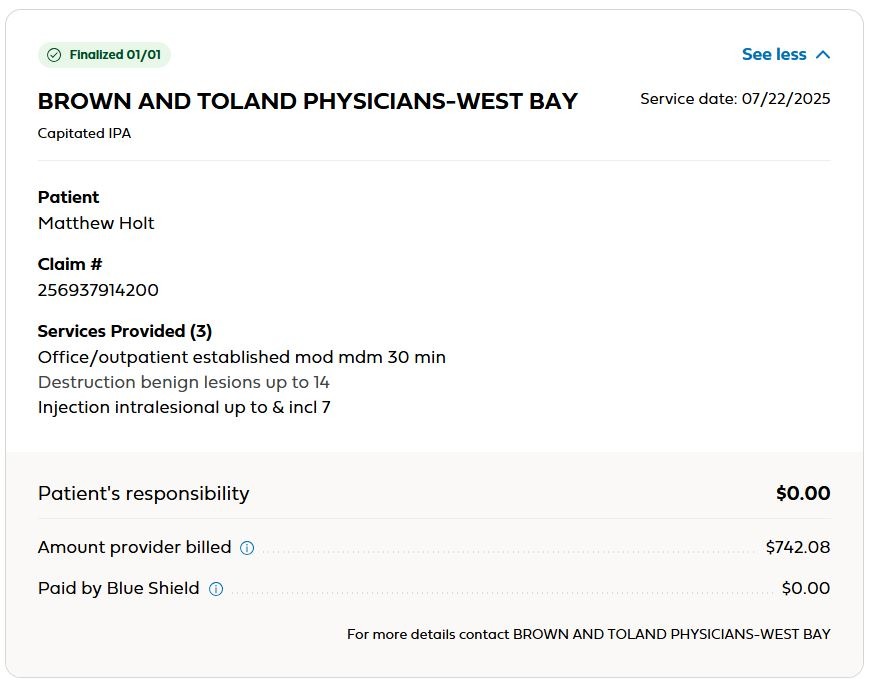

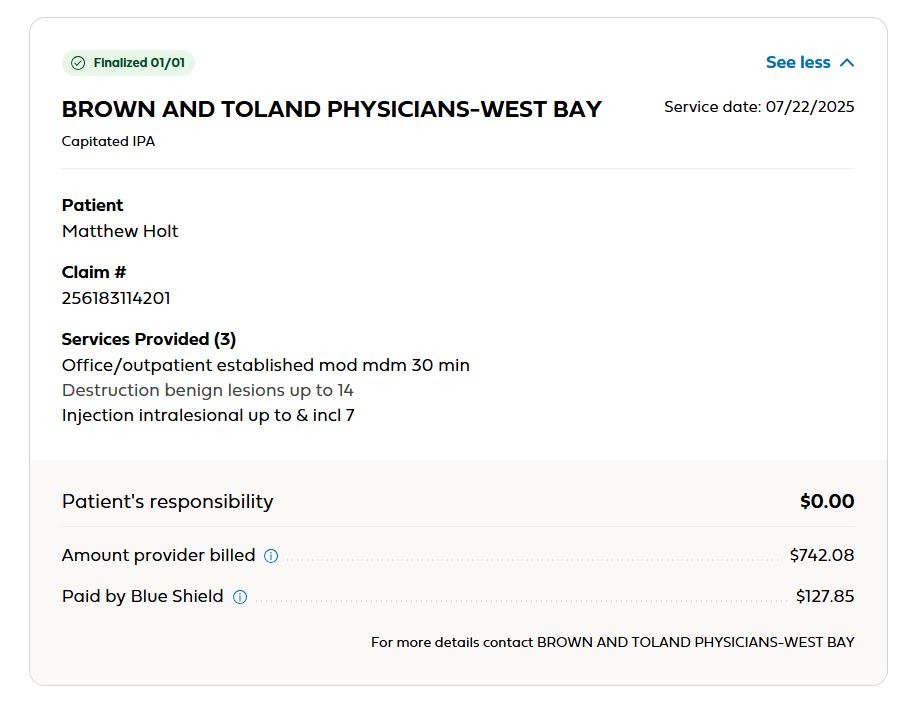

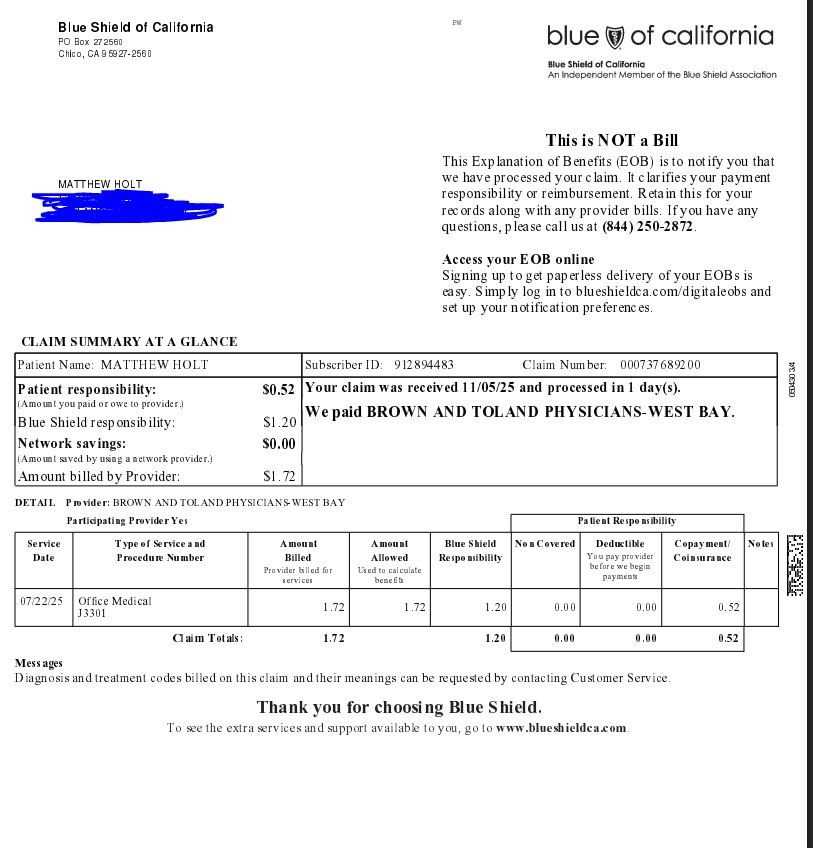

Then there’s one more for the same date (7/22/2026) which actually generated an actual PDF of an EOB presumably because Blue Shield thinks I owe something

Yes, there’s a claim for what seems to be the cost of the actual drug injected during the visit. A whopping $1.72. Blue Shield is not taking that lying down and only pays $1.20. The remaining 52 cents is somehow my responsibility–even though I paid a copay of $85 already. So somehow the drug being injected is billed outside the office visit.

I consulted the Blue Shield benefits summary which now shows that copay this year for specialists has gone up to $90 but it doesn’t mention co-insurance for in office drugs anywhere. Nor does anyone explain why it makes sense to bill $1.72 for any amount of a drug. However 52 cents is a shade over 30% of $1.72 and some Blue Shield HMO coinsurance (e.g. hospital stays) is billed to the patient at 30% of allowed charges, which is why you can meet your $12,000 out of pocket max, even though you are on an HMO. So it seems that this is co-insurance.

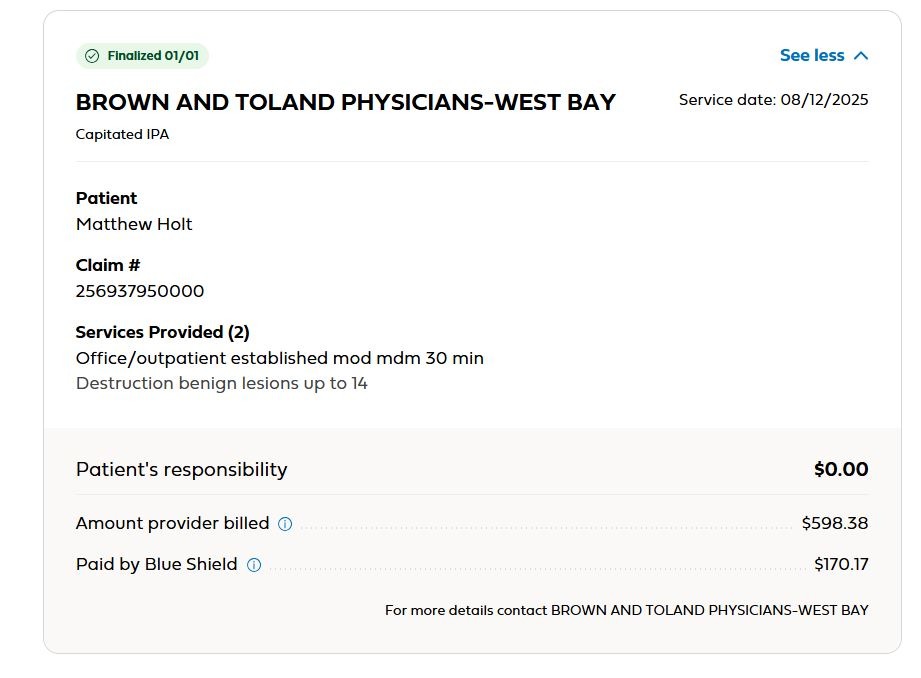

But while everyone (other than me!) seems to have agreed that I should pay 52 cents for the drugs injected during my July 22nd visit, it turns out that I also had basically identical visits earlier in July and August. For both of these I paid my copay of $85 and Blue Shield issued an EOB (the August one is below). Pacific Dermatology billed around $600 and got $170. I don’t know if my $85 was extra or part of the $170. If it’s the latter, then we paid equally for the visit.

Then we get to the visit in October. I again pay my $85 copay, and basically this is the visit that finally cures those lesions. Maybe it’s because I never went back, or maybe it’s some other obscure rule, but nearly 4 months later I got the bill for $51.96 in the mail.

Being me and being difficult, I called the billing service. I spoke to a very nice man called Terry Anderson who I assume is running an independent billing company. He told me that Brown & Toland, the Blue Shield of California-owned IPA managing me in the HMO, has massively increased their work by changing its systems but politely he avoided whining too, too much about them. Instead he told me that I owe coinsurance on their bill from my October visit. Why do I owe co-insurance whenI already paid a co-pay? He didn’t know and suggested I ask Brown & Toland. I told him I will….

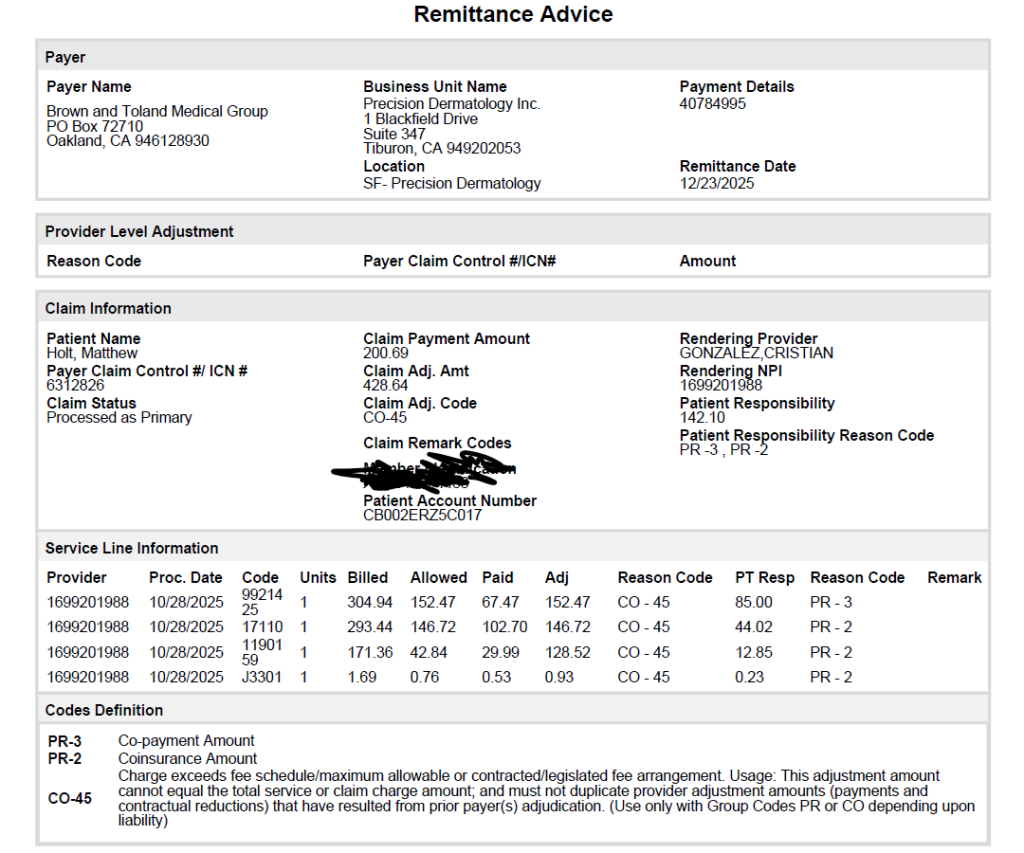

Meanwhile he sent me the EOB or remittance advice that Brown & Toland sent him.

If you compare this to the bill I was sent, you’ll see a few things. (I won’t send you back up to the page to the original bill, just trust me). The first is that the $304.94 charge for the office visit shown here doesn’t appear on the bill I got at all. Why not? Because it was settled completely and the billing service doesn’t think they are owed money, so they don’t put that in the bill to the patient. You’ll see that Blue Shield/Brown & Toland, adjusted the fee for that office visit down to $152.47 and paid $62.47. I paid my $85 co-pay which added to the $62.47 makes $152.47. So yes, I ended up paying more than Blue Shield did.

All the remaining three charges are also adjusted down. By cross referencing the bill we see that they were for

1) “Destruction of lesions” – $293.44 adjusted down to $146.72.

2) “Injection of the lesions” – $171.36 adjusted down to $42.84

3) The drug used in the injection – $1.69, adjusted down to 76 cents

However, this time around, Blue Shield/Brown & Toland did not pay the entire amount. Instead they paid 70% of the adjusted amount. So I have a 30% coinsurance payment. Same as if I had an inpatient visit.

You can rest assured that it’ll be a while before anyone gets the $51.96 out of me, but this does raise a few basic questions.

In each of the visits I met a PA who asked me about my condition, took a photo, then brought in Dr Gonzalez. He spent a max of 10 minutes with me, asking me about the lesions, then injecting and using dry ice on them. I am in no way complaining. That was all he needed to do and the lesions were healed. Mission accomplished

But a total of $330 received for a visit that took max 15 minutes, works out to ballpark $1250 an hour or roughly $187,500 per month (assuming 150 hours a month). So the physicians’ office, assuming it stays busy and collects a decent chunk of that, should be doing OK. And that’s not counting the cash based quasi-pharmaceuticals they and many other dermatologists sell directly. On the other hand it appears that they only got $127 or perhaps $255 for previous visits. So maybe they aren’t making that much. As I never got the full bill or the full EOB, how am I supposed to know?

But why Blue Shield/Brown & Toland allows them to bill three times for what’s basically one service is beyond me. And why are they billing different amounts for basically the same visit?

Or are they not, and it’s just hidden?

Why the drug in the injections is billed separately, when it’s an integrated part of the service, is also beyond me.

And why I am being charged a co-insurance for one of the four identical visits I made is also beyond me. (Yes, I will call Brown & Toland and ask…. But the Blue Shield EOB suggests I owe nothing).

And of course, there’s the consistent back and forth over the billing. Everywhere there are middlemen taking a cut. I assume the billing company is charging 5%+. The biller told me Brown & Toland puts its markup on it, and/or cuts a chunk off what it gets from Blue Shield–probably another 5%. And then there is the sheer cost of administration and figuring out who owes what, even if it’s 52 cents for a drug or $51.04 for an incorrectly billed co-insurance.

Then of course, there is the crass insanity of fee-for-service medicine. It’s completely in the doctor’s interest to keep me coming back to keep the cash till ringing. And it’s equally in the payer’s interest to stop it. It’s just the professionalism of Dr Gonzalez and the fact that I decided I was cured that stopped this process. But there’s no rationale for saying that the $1,000 spent (I think) to cure my lesions was the right number.

Bigger picture, this is a level of service that is essentially primary care. Obviously there is expertise in the diagnosis and expertise in the treatment. I am not suggesting that a dermatologist can be replaced by a primary care physician, but it seems to me that – like at Kaiser – a dermatologist with the ability to diagnose and treat minor dermatological issues could be part of a primary care based group. After all it was in all cases a 15 minute visit with no separate diagnostic test. Just another reason why we need Concierge Care for All.

And there is no world in which any of this is a rational way to fix my zits.

Matthew Holt is the Founder and publisher of THCB

Bengali (Bangladesh) ·

Bengali (Bangladesh) ·  English (United States) ·

English (United States) ·